Medicine HSN Code 3004: GST Rate, Exemptions & Classification

Understanding Medicine HSN Code 3004 is essential for pharmaceutical manufacturers, wholesalers, and healthcare businesses to ensure proper GST compliance. The 3004 HSN Code GST rate applies to finished medicaments that are ready for retail sale, including tablets, capsules, syrups, ointments, and injectables.

Correct classification under HSN Code 3004 helps businesses avoid tax errors, penalties, and compliance issues. In this guide, we break down the GST rate, exemptions, and classification framework to help you navigate medicine taxation in India efficiently.

What is HSN Code 3004?

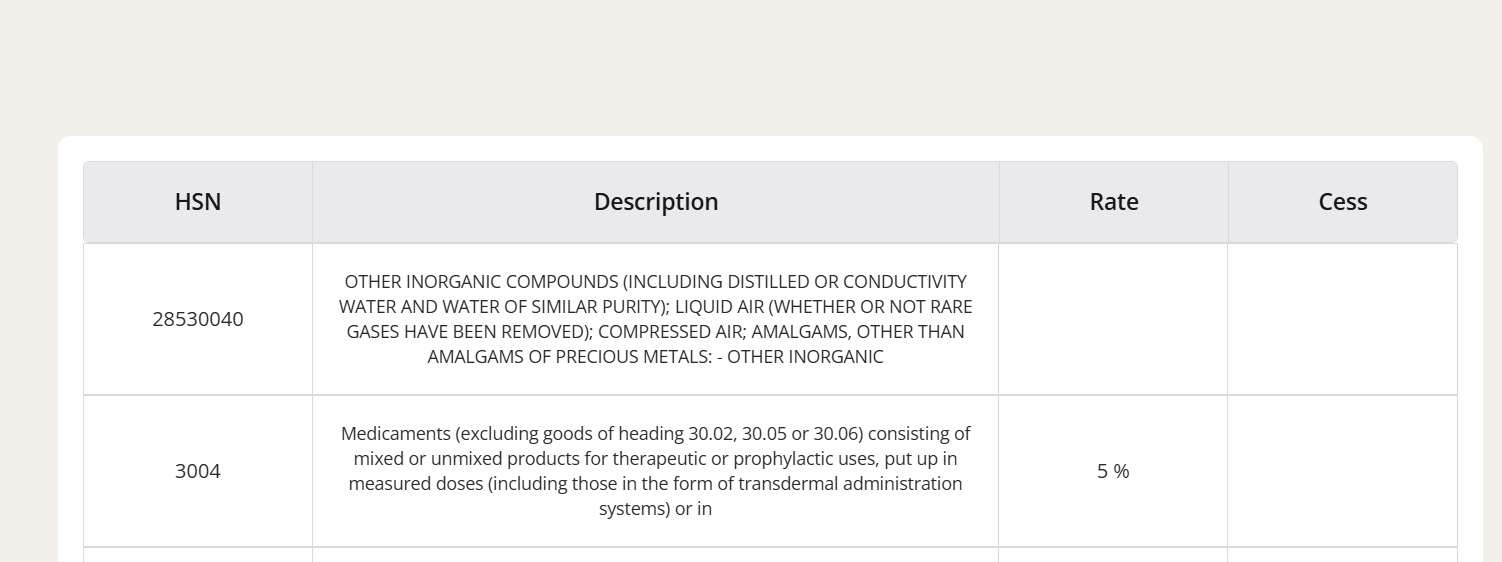

HSN Code 3004 applies to “Medicaments (excluding goods of headings 3002, 3005, or 3006), consisting of mixed or unmixed products for therapeutic or prophylactic uses.” Essentially, it covers all finished medicines that are manufactured, packaged, and ready for retail sale—whether allopathic, ayurvedic, homoeopathic, or veterinary.

This category includes tablets, capsules, syrups, ointments, injectables, and topical applications used for treating or preventing diseases.

GST Rates & Exemptions for Medicines under HSN Code 3004

Under the GST framework, the tax rates for medicines are determined by their importance in public healthcare and therapeutic use. After the 57th GST Council updates (effective 1 February 2026), several life-saving drugs remain GST-free, while essential and general medicines have updated GST slabs.

As per the latest GST revision, the Government of India continues to provide Nil GST on 33 critical life-saving medicines and 5% GST on essential healthcare products, while OTC and supplement products may attract 12–18% depending on classification.

Table Notes

- Most therapeutic and curative medicines are charged at 5% or 12%.

- Exemptions apply primarily to life-saving drugs, vaccines, and AYUSH formulations supplied under public health schemes.

- No compensation cess applies to medicines.

- Raw materials for bulk drugs may have separate GST rates (18%) depending on classification.

GST Rates Applicable Under 3004

What’s Included Under HSN 3004 Products?

This HSN covers all finished pharmaceutical formulations ready for direct consumption. That includes:

- Prescription allopathic medicines

- Traditional medicines (Ayurvedic, Unani, Homeopathic)

- Veterinary and preventive medicines

- Generic drugs, branded tablets, and syrups

Excluded from this category are items under headings:

- 3002: Sera and vaccines (biologicals)

- 3005: Wadding, gauze, and bandages

- 3006: Pharmaceutical goods used in hospitals

Explore Gimbooks HSN/SAC code & GST Rate finder

KKey Exemptions Under GST for Medicines

The Government continues to exempt several life-saving and government-supplied drugs to improve accessibility:

- Cancer, HIV/AIDS, and TB medications (Nil rated or 5%)

- COVID-19, Polio, and Measles vaccines (Nil rated)

- Drugs supplied under Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP)

- Medicines distributed through public hospitals and healthcare schemes

Recent Exemptions (Post-February 2026)

- GST remains Nil on 33 life-saving drugs treating cancer, renal disorders, epilepsy, and heart conditions.

- GST remains 5% for additional essential medicines under public health programs.

Input Tax Credit (ITC) Rules for Medicines

Registered manufacturers, distributors, and pharmacies can claim ITC for GST paid on raw materials, packaging materials, and logistics services used in producing and distributing taxable medicines. However:

- ITC cannot be claimed for medicines sold under GST-exempt or Nil-rated categories.

- Businesses dealing in both taxable and exempt drugs must maintain separate accounting to ensure compliance under Section 17 of the CGST Act.

GST on Medicine Billing: Practical Scenarios

- A pharmacy selling antibiotics (12% GST) can claim ITC on invoices from manufacturers or wholesalers.

- A government supply distributor invoicing cancer drugs (0% GST) cannot claim ITC on inputs.

- Ayurvedic manufacturers under the AYUSH Ministry charge 12% GST on formulations but can claim ITC on herbal ingredients.

Common Mistakes in Medicine GST Filing

- Incorrect HSN use for biologicals (should be 3002, not 3004).

- Claiming ITC for exempted life-saving drugs.

- Calculating GST over marked MRP (GST is already included in printed MRP).

- Not segregating mixed sales (taxable vs non-taxable) in GST returns.

Conclusion

HSN Code 3004 standardizes classification and GST compliance for finished medicines and pharmaceutical formulations. With revised rates in 2026 providing Nil to 12% GST depending on category, the system balances affordability for patients and compliance simplicity for healthcare businesses. Medical suppliers and distributors should stay updated on GST Council notifications to ensure accurate billing, reporting, and ITC claims.

Also explore

FAQs: HSN Code 3004 & Medicine GST

What is HSN 3004?

HSN 3004 includes finished medicaments in measured doses (tablets, syrups, capsules) used for therapeutic or preventive purposes.

What is the GST rate for medicines under HSN 3004?

As of 2026, GST on medicines ranges from 0% (exempt) for life-saving drugs, 5% for essential medicines, and 12% for general medicines and formulations.

Are traditional medicines like Ayurvedic or Homeopathic taxed?

Yes, Ayurvedic, Unani, Siddha, and Homeopathic medicines are taxed at 12% under HSN 3004.

What is the HSN code for ayurvedic medicines?

Ayurvedic medicines generally fall under HSN Code 3004 if they are manufactured, packaged, and labeled for therapeutic or preventive use under GST regulations in India. The applicable GST rate depends on the product classification and formulation.

Can Input Tax Credit be claimed on medicine supplies?

ITC is available only for taxable categories (5% or 12%) and not for Nil-rated or exempted medicines.

Which life-saving drugs are GST-exempt?

Cancer, HIV/AIDS, TB drugs, vaccines, and medicines under government schemes such as PMBJP are exempt from GST.

What is the tax on medicine in India?

The tax on medicine in India is charged under GST and usually ranges between 5%, 12%, or 18%, depending on the type and classification of the medicine. Most essential and life-saving drugs are taxed at 5%, while certain formulations may attract higher GST rates.