Manufacturing Services HSN Code 9988 and GST Rates [2026]

Understanding Manufacturing Services HSN Code 9988 is crucial for businesses engaged in job work or contract manufacturing. The 9988 HSN code GST rate determines how GST is applied to services where a manufacturer processes, assembles, or handles goods owned by another party. Knowing the job work HSN code or job work SAC code helps companies comply with tax regulations and ensures smooth invoicing for processing, finishing, or packaging services.

What is HSN Code 9988?

HSN Code 9988 covers “Manufacturing Services on Physical Inputs (Goods) Owned by Others.”

This includes all forms of job work or contract manufacturing, where a registered manufacturer (the job worker) performs processing, assembly, or production on inputs or goods owned by another person (the principal manufacturer).

In simple terms, any service provider performing processing, finishing, fabrication, or packaging of goods that belong to someone else falls under this SAC code. The 9988 HSN code GST rate naturally varies depending on the type of job work or goods involved, as specified under GST regulations.

Common examples are:

- Textile dyeing, stitching, or printing services

- Vehicle body-building services

- Goldsmith services for jewelry fabrication

- Leather tanning or cutting work

- Processing of raw materials like steel, plastics, or rubber under contract

GST Rates & Exemptions for HSN Code 9988 (2026 Clarification)

Under GST, services under HSN/SAC 9988 can attract 1.5%, 5%, 12%, or 18% GST, depending on the type of manufacturing activity and government notifications.

The standard GST rate for most job work services stands at 18% (continues in 2026) after the rationalization of earlier 12% rates. Certain industries continue to enjoy concessional rates (5% or 12%) based on their classification under the Customs Tariff Act and specific GST notifications.

2026 Important Clarification:

- If a job work activity does not fall under any specific concessional notification entry, 18% GST applies by default.

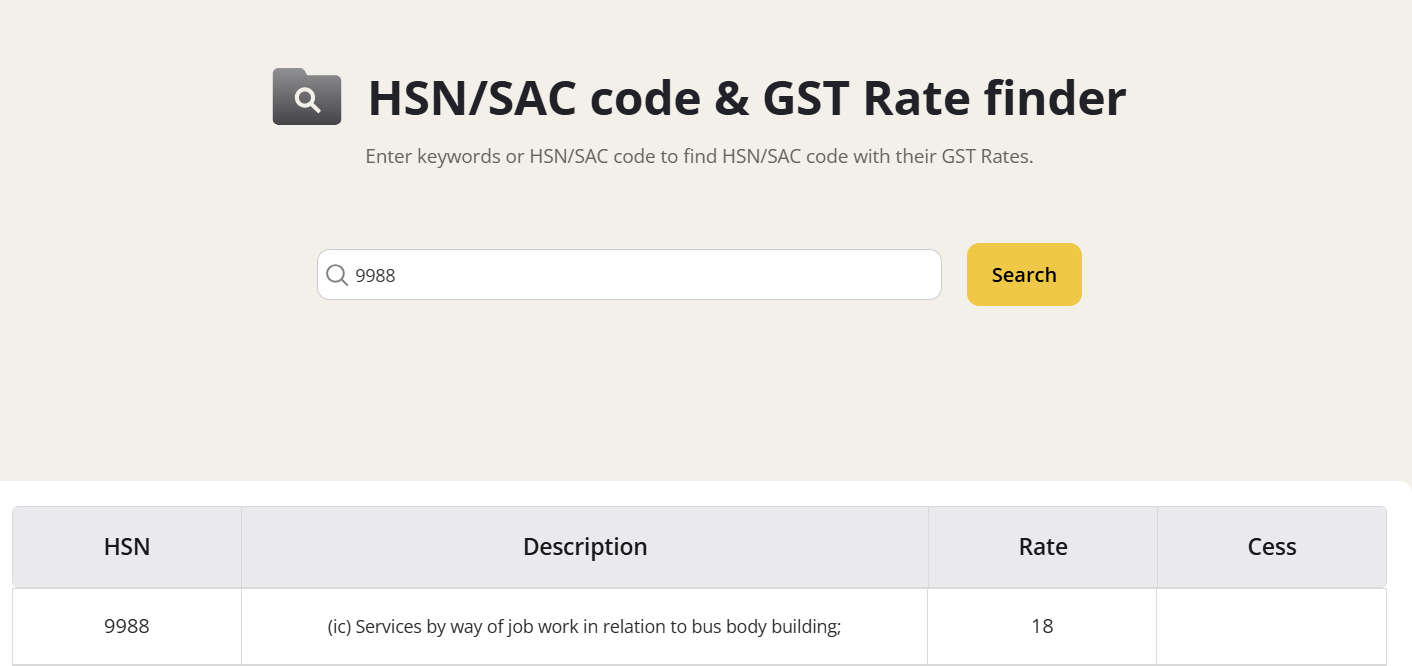

- Bus body building, heavy fabrication, electronics manufacturing, and machinery processing continue under 18% GST.

- Textile and apparel job work remains at 5%, subject to conditions under Notification 11/2017 (as amended up to 2026).

Table Notes

- The rate structure under SAC 9988 is activity-based, not uniform.

- Services involving food, textile, jewelry, printing, and leather generally attract lower rates (5% or 12%).

- Heavy industries and mechanical or electronic manufacturing fall under 18%.

- No compensation cess applies to any job work or manufacturing services.

GST Rates Applicable Under 9988

(Updated as per GST Notification and Job Work Rate Revision, September 2025).

What’s Included Under HSN 9988 Manufacturing Services?

SAC 9988 primarily includes processing services where the raw materials or semi-finished goods are owned by the client (principal), and manufacturing or finishing work is carried out by another person (the job worker). Key inclusions:

- Textile & Apparel Processing – dyeing, cutting, sewing, or embroidery

- Engineering & Fabrication – metal treatment, welding, or component assembly

- Printing & Packaging Work – newspapers, stationery, or branded labels

- Food & Beverage Processing – milling, packing, and quality testing

- Pharma & Chemical Processing – blending, bottling, and compounding

Such manufacturing is treated as a service under GST, not a goods supply.

Explore Gimbooks HSN/SAC code & GST Rate finder

Key Exemptions Under GST for Manufacturing Services

Certain manufacturing and job work services are exempt or attract reduced GST rates to promote primary sector and MSME growth:

Input Tax Credit (ITC) Rules for Manufacturing & Job Work (2026 Update)

Under GST law (Sections 19 & 143 of the CGST Act read with Rule 45 of CGST Rules), both the principal manufacturer and the job worker can claim Input Tax Credit (ITC) on inputs, capital goods, and input services used for job work, subject to prescribed conditions.

ITC Eligibility

- The principal manufacturer can claim ITC on inputs or capital goods sent to a job worker, even if goods are directly dispatched to the job worker’s premises.

- Inputs must be returned to the principal (or supplied from the job worker’s premises) within:

- 1 year for inputs

- 3 years for capital goods

- Registered job workers can claim ITC on input services (such as electricity, repair, or subcontracting services) used for processing.

- Filing of Form GST ITC-04 is mandatory for reporting goods sent to and received from job workers (filed half-yearly as per current compliance rules).

- E-way bill compliance is required where applicable for movement of goods.

ITC Restrictions

- ITC is not available for goods or services used for personal or non-business purposes.

- If goods are not returned within the prescribed 1-year or 3-year period, the transaction is treated as deemed supply from the date they were originally sent. GST becomes payable along with applicable interest.

- Proper documentation (delivery challan, job work agreement, and records of movement) must be maintained to avoid disputes during GST audits.

Example (2026 Practical Scenario)

If a textile company sends raw fabric worth ₹5,00,000 to a registered job worker for dyeing, and the job worker charges ₹50,000 + GST at 5% (₹2,500), the textile company can claim ITC of ₹2,500 on the job work charges.

However, the finished goods must be received back (or supplied from the job worker’s premises) within 1 year to retain ITC eligibility and avoid tax liability under deemed supply provisions.

GST on Manufacturing Services: Practical Scenarios (2026 Status)

The following examples remain valid under the 2026 GST structure:

- Metal fabrication under SAC 9988 → 18% GST

- Tailoring services under SAC 9988 → 5% GST

- Dairy or food product contract processing → generally 18% unless specifically exempt

- Jewellery job work → 5%–12% depending on classification

No major rate overhaul has been announced for SAC 9988 in the 2026 GST Council updates.

Common Mistakes in Manufacturing Services GST

- Using wrong SAC codes (mixing 9988 with trading or repair service categories).

- Charging a flat 18% rate instead of checking concessional job work rates.

- Delayed submission of ITC-04 forms tracking material flow.

- Claiming ITC for goods not returned within the allowed period.

- Misclassifying job work as the supply of goods instead of services.

Conclusion

HSN Code 9988 continues to provide a structured classification for job work and contract manufacturing services across industries — from textiles and handicrafts to engineering and heavy machinery. Under the 2026 GST framework, applicable rates generally range between 5% and 18%, with 18% as the default rate where no concessional notification applies. Clear ITC eligibility provisions, mandatory ITC-04 compliance, and e-invoicing (where applicable) make accurate SAC classification and documentation essential for staying audit-ready and avoiding interest or penalty exposure.

Businesses must ensure correct SAC reporting, timely return of goods sent for job work, and proper GST filings to maintain seamless compliance in 2026.

Also explore

FAQs: Manufacturing Services under HSN 9988

What is HSN 9988?

HSN 9988 refers to manufacturing or processing services on physical inputs owned by others, commonly known as job work under GST. It covers a wide range of industries, including textiles, leather, food processing, machinery, and chemicals.

What is the GST rate for SAC 9988 manufacturing services?

The GST rate varies by service type:

- 0% – Agriculture-related job work (fruits, vegetables, basic food products, animal feed).

- 5% – Textiles, books, leather items, tailoring, and other basic manufacturing.

- 12% – Special cases like umbrella manufacturing or processed jewellery.

- 18% – General and industrial manufacturing (machinery, electronics, vehicles, chemicals, plastics, etc.).

Can job workers claim ITC?

Yes. Both job workers and principal manufacturers can claim Input Tax Credit (ITC) under Sections 19 & 143 of the CGST Act, subject to:

- Proper documentation and accounting in Form GST ITC-04.

- Inputs being returned to the principal within 1 year (for inputs) or 3 years (for capital goods).

- Services used for processing being directly related to business activities.

Is tailoring considered a manufacturing service?

Yes. Tailoring is classified under SAC 9988 and is generally taxed at 5% GST, falling under textiles and readymade garment manufacturing.

What happens if goods sent for job work aren’t returned?

If goods are not returned within the prescribed period, they are treated as a deemed supply, and GST becomes payable by the principal manufacturer on the value of the goods.

What is the job work HSN code?

The job work HSN/SAC code is 9988, covering services on goods owned by others. It specifies GST rates for processing, assembly, contract manufacturing, and other outsourced production activities.